Outrageous Predictions

Carry trade unwind brings USD/JPY to 100 and Japan’s next asset bubble

Charu Chanana

Chief Investment Strategist

A Trump-driven Fed pivot crashes the carry trade, hurling USD/JPY to 100 and unleashing Japan’s wild...

Investment and Options Strategist

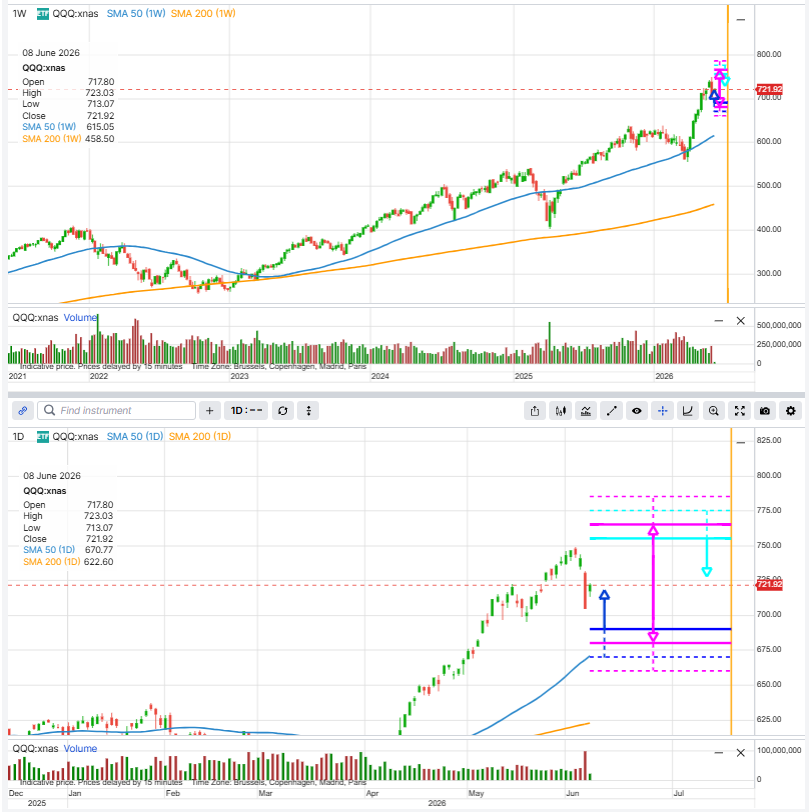

Summary: The Nasdaq had a sharp selloff last week, and QQQ is bouncing back. But is it a recovery, a range-bound consolidation, or a dead-cat bounce before the next leg lower? The options market won’t tell you the answer directly, but it does give you a framework.

Rebound, range, or dead-cat bounce? How traders can use expected move to structure uncertainty.

After a sharp selloff, the first rebound often creates more questions than answers. Is the market recovering, or is it merely catching its breath before another leg lower? For investors looking at the Nasdaq through QQQ, that uncertainty is exactly where options can be useful.

The goal is not to predict the next move perfectly. The goal is to choose a strategy that matches your view.

For this educational example, we use QQQ options expiring on 17 July 2026. That expiry gives the trade roughly six weeks to develop: long enough to avoid turning every intraday move into a crisis, but short enough for option premium and time decay to remain meaningful. Very short-dated options can be tempting after a volatility spike, but they are often harder to manage because gamma risk rises quickly as expiration approaches.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

Before choosing strikes, we need a reference point. One useful method is the at-the-money straddle. Around the time of the screenshots, QQQ traded near 722, while the 723 call was priced around 23.04 and the 723 put around 21.03. Together, that straddle cost about 44 points.

Method note: The at-the-money straddle is often used as a practical proxy for the market’s expected move because it combines the price of an at-the-money call and an at-the-money put with the same expiry. Since the position is direction-neutral at the start, its total premium reflects how much movement option buyers are paying for, and option sellers are demanding compensation for, before expiration. It should not be read as a forecast or guaranteed range, but as a market-implied reference point for thinking about strike selection.

That does not mean QQQ must move 44 points. It means the options market was pricing a rough expected range of about 679 to 767 by expiration. This range can help traders think more clearly about strike selection. Instead of randomly choosing strikes that “look far away,” we can place strategies around the market’s own implied range.

QQQ rebounded after Friday’s selloff, but the option strikes frame three possible paths: recovery, range, or renewed weakness. Source: SaxoTrader

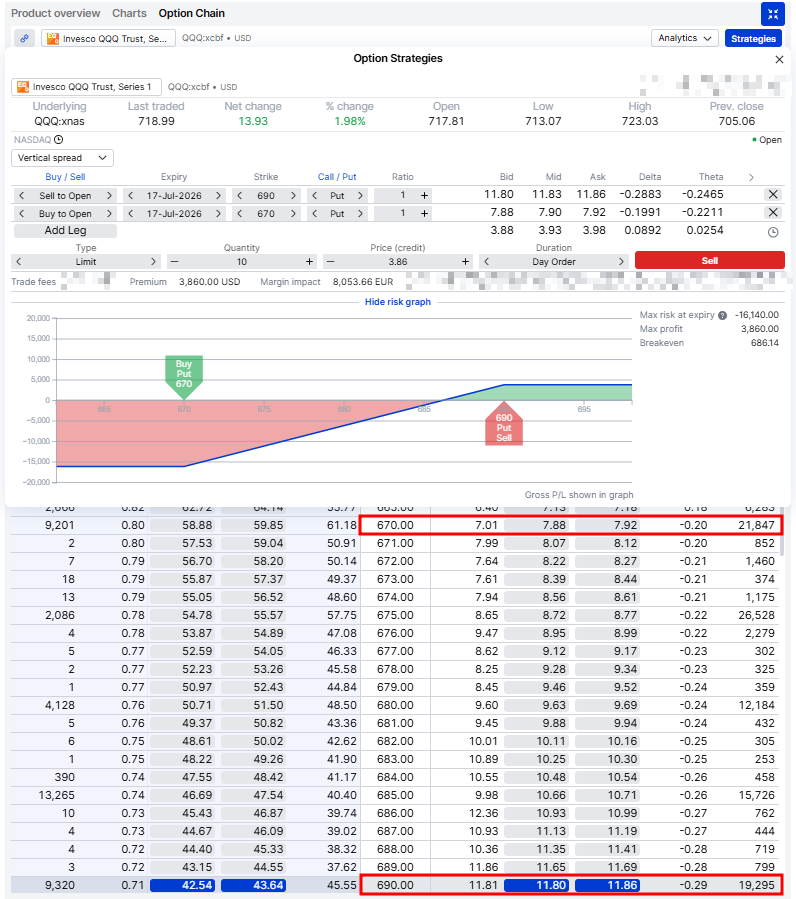

1. Bullish view: the rebound can hold

A trader with a constructive view may believe the selloff was sharp but temporary. In that case, the market does not necessarily need to surge higher. It may simply need to avoid falling back below a key level.

One way to express that view is a bull put spread.

In the screenshot, the example sells the 690 put and buys the 670 put, both expiring 17 July 2026. The spread receives a credit of about 3.86 points. Since QQQ options represent 100 shares, that is about 386 dollars per spread before costs. The maximum risk is the 20-point spread width minus the credit received, or about 1,614 dollars per spread.

A bull put spread can express a constructive view without requiring QQQ to rally sharply. Source: SaxoTrader

The short 690 put is above the lower edge of the expected-move range, but still below the market price. That makes the position bullish, but not wildly so. The trader is effectively saying: “QQQ may fluctuate, but I expect it to stay above 690.”

The advantage is that the trade can work if QQQ rises, moves sideways, or even slips moderately. The disadvantage is that the profit is capped at the credit received, while a renewed selloff below 690 can pressure the position quickly. There is also assignment risk with ETF options if short options are held near expiration and finish in the money.

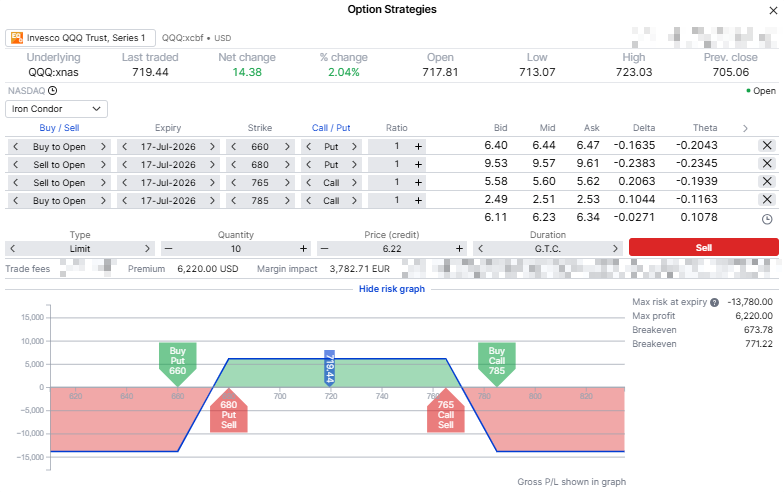

A neutral trader may believe the market needs time to process the selloff and rebound. QQQ may not collapse, but it may also struggle to immediately resume its previous trend.

For that view, an iron condor can be useful.

The example uses four legs, all expiring 17 July 2026: buy the 660 put, sell the 680 put, sell the 765 call, and buy the 785 call. The position receives a credit of about 6.22 points, or roughly 622 dollars per iron condor before costs. With 20-point-wide wings, the maximum risk is about 1,378 dollars per spread.

The iron condor turns a range-bound view into a defined-risk options structure. Source: SaxoTrader

The short strikes at 680 and 765 sit close to the expected-move range. That is the key educational point. The trader is not choosing a random range. The structure is built around what the options market is already implying.

The trade benefits if QQQ remains between the short strikes and time decay works in the trader’s favour. It may also benefit if implied volatility falls after the volatility spike.

But neutral does not mean safe. If QQQ breaks below 680 or above 765, the trade becomes directional very quickly. That is why defined-risk wings matter. They limit the damage if the market does something inconvenient, which markets occasionally do, just to keep us humble.

A broader index, such as XSP or SPX, could also be considered for this type of neutral strategy. A broader index is usually less concentrated than QQQ and may therefore be easier to manage for investors who do not want a Nasdaq-heavy exposure.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

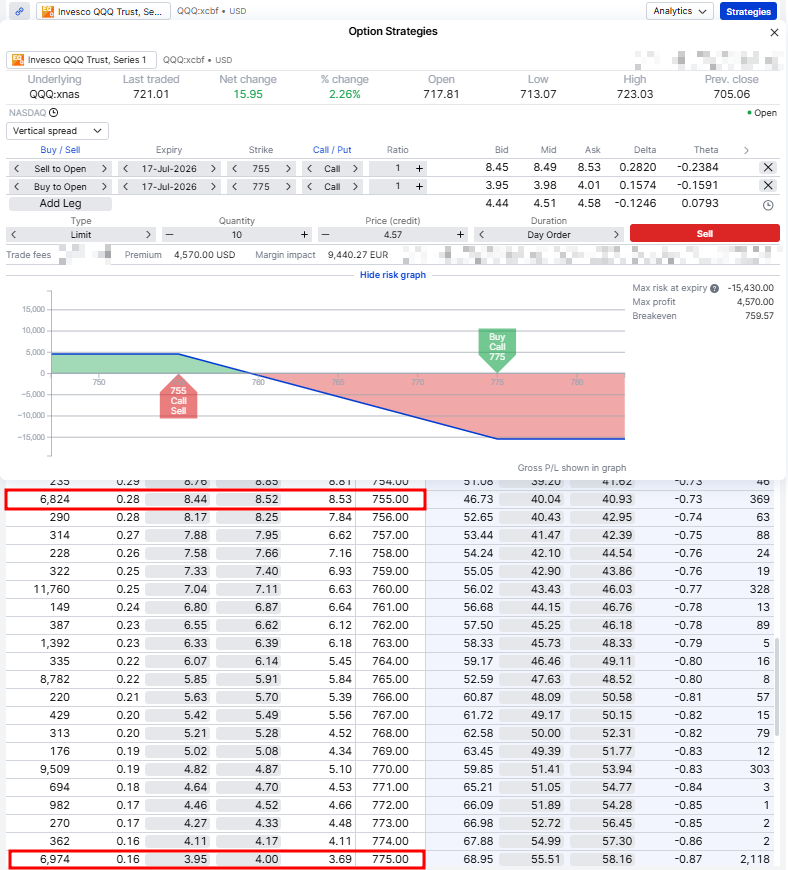

A bearish trader may see the rebound as a relief rally rather than a full recovery. Instead of buying puts after a volatility spike, another approach is to sell upside premium through a bear call spread.

The example sells the 755 call and buys the 775 call, expiring 17 July 2026. The spread receives a credit of about 4.57 points, or roughly 457 dollars per spread before costs. The maximum risk is about 1,543 dollars per spread.

A bear call spread can express the view that the rebound fades before QQQ pushes much higher. Source: SaxoTrader

The short 755 call is below the upper edge of the expected-move range. This gives QQQ some room to continue bouncing, but the trade assumes that upside momentum eventually stalls before QQQ moves much beyond 755.

The advantage is that the position has defined risk and can profit if QQQ moves sideways or lower. The disadvantage is that a stronger rebound can hurt quickly. A trader may be right that the market is fragile, but still lose money if the entry is too early or the short strike is too close.

Options are not only about leverage. They are also a way to structure uncertainty.

A bullish trader might use the 690/670 bull put spread. A neutral trader might use the 680/660 and 765/785 iron condor. A bearish trader might use the 755/775 bear call spread.

Same underlying. Same expiry. Three different views.

That is the real lesson: do not start with the option strategy. Start with the market view, then choose the structure that fits it.

| Related articles/content |

|---|

| What IV crush really means in practice reviewed version | 9 April 2026 Trading earnings with defined | 31 Mar 2026 PayPal earnings trading the expected move with options | 4 May 2026 ArcelorMittal earnings what a 10 options move can teach traders | 28 April 2026 ASML earnings is the 8 move already priced in | 10 April 2026 ASML earnings - how to think about the setup before the numbers | 10 April 2026 Options Brief - Mag 7 earnings night Fed holds - 29 April 2026 Options Brief - Mag 7 earnings on deck - 28 April 2026 Options Brief - Oil jolt - US records - 23 April 2026 |

| More from the author |

|---|

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy