Quarterly Outlook

Q3 Investor Outlook: Beyond American shores – why diversification is your strongest ally

Jacob Falkencrone

Global Head of Investment Strategy

Global Market Quick Take: Asia – July 22, 2025

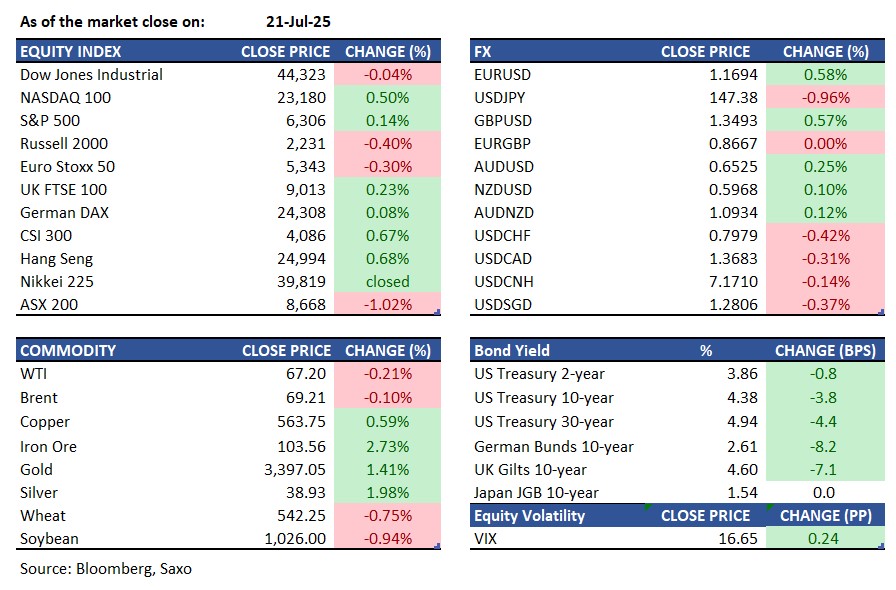

Key points:

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

Equities:

Earnings this week:

FX:

Economic calendar: Australia Central Bank Minutes; Mexico Retail Sales, International Reserves; New Zealand Trade Data; Taiwan Export Orders, Jobless Rate; US Richmond Fed Manufacturing Index.

Commodities:

Fixed income:

For a global look at markets – go to Inspiration.

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Global Head of Investment Strategy

Quarterly Outlook

Global Head of Macro Strategy

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Chief Investment Strategist

Quarterly Outlook

Head of Commodity Strategy