Key points:

- Macro: U.S. jobless claims fall, indicating strong job market conditions

- Equities: US markets reach new highs on strong earnings

- FX: USD strengthens to 98.95; positive US data; safe-havens JPY and CHF decline

- Commodities: Oil rallies while copper remains subdued

- Fixed income: Canada led a rise in foreign interest in U.S. government securities

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

- Retail sales rose by 0.6% in June, surpassing nearly all predictions from a Bloomberg survey of economists. Out of 13 categories, 10 saw growth, with motor vehicle sales rebounding after two consecutive months of decline. This increase occurred even though administrative data indicated car sales fell during June.

- U.S. unemployment benefit applications fell for the fifth consecutive week, reaching their lowest point since mid-April, indicating a strong job market. Initial jobless claims dropped by 7,000 to 221,000 for the week ending July 12, surpassing the median forecast of 233,000 applications from a Bloomberg survey of economists.

- Philly Fed Index surges to 15.9 in July, beating expectations of –1, indicating manufacturing activity expanded.

- US Congress passed the first federal legislation to regulate stablecoins.

Equities:

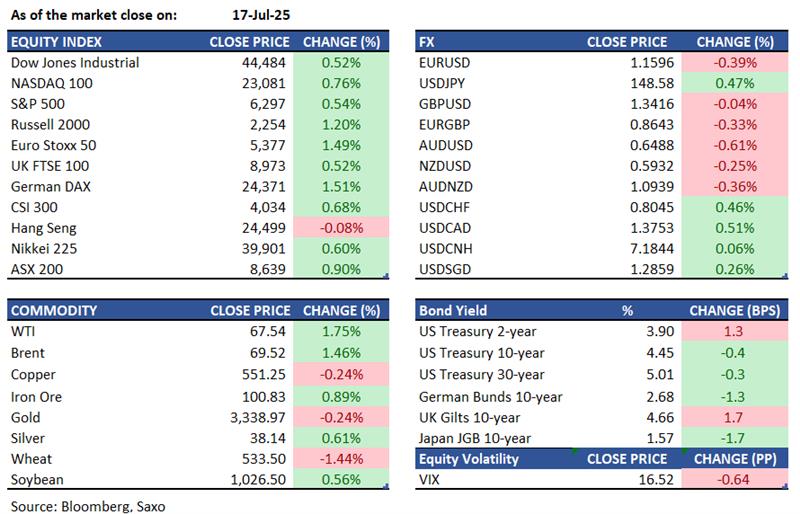

- US - US stocks rose as positive earnings and strong economic data pushed indexes toward new highs. The S&P 500 and Nasdaq 100 gained 0.5% and 0.7%, respectively, while the Dow Jones added 230 points, or 0.5%. June retail sales grew 0.6%, surpassing expectations and showing consumer resilience amid tariff concerns. Jobless claims fell to 221,000, the lowest in three months, indicating a strong labor market. United Airlines and PepsiCo led earnings gains with shares up 3.1% and 7.4%. TSMC jumped 3.9% on record profits, boosting chip stocks like Nvidia (+0.9%) and Marvell (+1.6%). Netflix reported after the close and beat expectations across revenue, net profit and operating margin reached 34.1% from 27.2% last year. It is down 1.8% in after-hours trading.

- EU - European stocks surged on Thursday, erasing losses from the previous three sessions as markets evaluated corporate returns and trade outlooks. The Eurozone's STOXX 50 climbed 1.6% to 5,370, and the STOXX 600 rose 1% to 547. Schneider Electric led Eurozone gains, soaring 7.7% on news of potentially acquiring Temasek’s stake in its Indian subsidiary. ASML increased 3.9% after its previous day’s decline due to pessimistic guidance. Banks and tech stocks also rose. Nordea fell 2.7% after disappointing profits. Outside the Eurozone, ABB jumped 9.9% on record orders, while Novartis dropped nearly 2% despite beating profit expectations and announcing a $10 billion buyback.

- HK - HSI fell 0.1% to 24,499, its second straight decline, due to profit-taking post-recent highs and U.S. futures' dip before retail sales data. Concerns about U.S. tariffs persisted after President Trump's announcement to over 150 countries. Financial stocks dropped, while auto stocks rose after China moved to address competition in the EV sector, with Li Auto (9.5%), Geely Auto (3.9%), and Nio (7%).

Earnings this week:

- Friday: 3M (MMM), American Express (AXP), Charles Schwab (SCHW).

FX:

- USD regained strength after initial reports that President Trump might fire Fed Chair Powell were rebutted and deemed unlikely. Positive US data, including strong Retail Sales and a drop in jobless claims, supported the Dollar's recovery to a session high of 98.95.

- UK and Australian job reports were disappointing, but GBP performed well, trading around 1.3410. AUDUSD bounced back to its 50-day moving average after reaching lows of 0.6455.

- Safe-haven currencies like the CHF and JPY saw declines, with concerns over Fed independence. USDJPY and USDCHF traded higher at 148.70 and 0.8050, respectively.

- Economic calendar – US Building Permits Preliminary, US Housing Starts, Us Michigan Consumer Sentiment Preliminary

Commodities:

- Oil prices held steady as U.S. data showed economic resilience despite trade war impacts, with market signals suggesting tightening crude supply. WTI hovered just below $68 following a 2% increase, while Brent neared $70.

- Copper prices in London rose slightly as Chinese buyers began to replenish tight inventories, despite remaining below highs seen after President Trump's tariff announcement. Recent large exports of copper to the U.S. have led some Chinese manufacturers to seek lower buying opportunities.

Fixed income:

- Treasuries saw significant early volatility but settled with 2-year yields up by about 3 basis points and the rest of the curve slightly lower. Dollar swap spreads widened due to increased paying flows. In May, foreign demand for U.S. government securities surged, led by Canada, which bought $65.8 billion in Treasuries, reaching a record $430 billion in total holdings.

For a global look at markets – go to Inspiration.