Outrageous Predictions

Executive Summary: Outrageous Predictions 2026

Saxo Group

Read Saxo's Outrageous Predictions for 2026, our latest batch of low probability, but high impact ev...

Chief Investment Strategist

This content is marketing material.

Here’s a snapshot of the most important questions — and the views we discussed.

We’ve probably seen peak tariff rates, but not peak tariff uncertainty. The effective average tariff rate has already jumped from 2.5% to something over 20% — the highest levels since the 1930s. For now, the hard data still reflects the impact of front-loaded demand, as companies and consumers rushed to buy goods ahead of expected tariff increases.

But that’s only the first phase.

We haven’t yet seen the real data showing the drag from sustained uncertainty and elevated tariff costs. As that uncertainty filters through business decisions, we expect a more meaningful slowdown in real economic activity — in production, hiring, and investment. In short, the rate shock may be behind us, but the real growth damage is just starting to unfold.

They are incredibly ambitious — and highly unrealistic on traditional timelines. According to the Wall Street Journal, Trump’s team is targeting six bilateral trade deals per week, while historically it can take several years just to finalize a single agreement. And it’s not just about cutting headline tariff rates. Each agreement would need to cover a wide range of sensitive areas — tariffs, non-tariff barriers, rules of origin, and digital trade frameworks — all of which normally require painstaking negotiations across legal, regulatory, and political lines.

Trade deals are complex because they don't just settle market access; they also require dispute mechanisms, enforcement standards, and mutual trust — none of which can be fast-tracked easily. Attempting to negotiate dozens of such deals simultaneously would mark a major break from past trade strategies, making it look incredibly ambitious.

Tariffs act like a tax on trade — raising costs for companies, disrupting supply chains, and ultimately weighing on growth. In the short term, businesses may try to front-load imports ahead of tariff hikes, temporarily boosting demand. But as time passes, higher input costs squeeze corporate margins, consumer prices rise, and competitiveness erodes.

Companies that can’t pass on costs may cut investment or lay off workers. Over time, the impact of tariffs compounds into slower economic activity, weaker earnings, and a more fragile labor market. While tariffs can cause a one-off bump in inflation as prices reset, they are far more damaging to growth than to long-term inflation dynamics.

The Fed is stuck in wait-and-see mode — and likely won’t move until the hard data turns. One of the hardest parts of the last three years has been navigating the gap between soft data (surveys, sentiment) and hard data (employment, consumption). Right now, we’re seeing peripheral data weaken — from manufacturing to trade — but the big headline numbers still look relatively resilient.

Tariffs raise the odds of a Fed response eventually, but perhaps more slowly than markets expect. The labor market, a key Fed focus, is a lagging indicator. On top of that, we’re seeing front-loading of demand — by manufacturers, industrials, and even consumers — which could make data from March through June look stronger than the underlying trend really is.

The Fed is very cautious about acting preemptively, especially after the April 2–3 tariff escalation. Imagine if they had rushed to cut rates in early April — only to see the situation change dramatically days later with a 90-day pause and China returning to talks. The risk of looking politically reactive is too high.

So unless the hard data — particularly jobs and consumption — clearly rolls over, the Fed is unlikely to act before July. They need real deterioration to justify a move, not just forecasts or soft indicators.

Corporates now face two choices: raise prices or take a hit on margins. With consumers far more constrained today than in 2020 — without the fiscal stimulus and excess savings cushion — the more likely outcome is margin compression. Companies like Walmart have already made it clear: passing on higher costs to consumers is much harder in the current environment.

We started 2025 with expectations of around 13% earnings growth for the S&P 500. But with a roughly 5 percentage point increase in average tariff rates, that picture looks increasingly unrealistic. Historical sensitivity analysis suggests a 5pp tariff increase could directly reduce S&P 500 EPS growth by about 2%. Adding broader pressures from slower demand and margin erosion, the overall hit could be closer to 8-10%. That would leave earnings growth expectations at around 3-5% — a major step down from where forecasts began the year.

In short, tariffs aren’t just a tax on trade — they’re setting up a significant drag on corporate profitability, with ripple effects likely to reach the labor market next.

Yes — and the risks are rising. The tone around tariffs and the Fed has softened, but the underlying fundamentals haven’t improved. Policy uncertainty remains high, meaningful stimulus still looks distant, and valuations are still uncomfortably rich. Meanwhile, fund managers are rotating aggressively out of U.S. assets.

On earnings, the situation is deteriorating, as discussed above. At the same time, valuations are still stretched. The S&P 500’s forward P/E remains one standard deviation above its 10-year average. So we are now staring at a brutal combination: falling earnings estimates and a market that should logically demand a higher risk premium — meaning lower P/E multiples ahead. This is not a setup that supports high index levels.

Technically, the S&P 500 remains vulnerable as long as it trades below its 200-day moving average, currently around 5,747. Until the index can reclaim that level convincingly, the path of least resistance remains to the downside.

It’s definitely getting murkier. Structurally, the U.S. still holds enormous advantages — and there are no true alternatives yet to the technology, innovation, strength of balance sheets, global dominance, and pricing power of its leading companies.

Try finding an alternative to Microsoft or Amazon in cloud computing, Google in search, Meta in social media, or Nvidia in chips — it’s not easy. Similarly, the depth of U.S. financial markets, the availability of capital, and the global influence of U.S. tech platforms remain unmatched.

That said, the perception of U.S. invincibility is being challenged. Rising fiscal deficits, political volatility, threats to institutional independence, and attempts to politicize monetary policy are all clouding the picture. The structural strengths of the U.S. remain real — but investors are starting to price in the idea that U.S. assets may no longer be a risk-free anchor in a fragmented global system.

The setup for the Mag 7 is tricky. On paper, valuations have compressed back to 2022 levels, and technical indicators suggest the group has entered oversold territory. But those two conditions alone aren’t enough. Without a clear positive catalyst, it's hard to argue for a durable rebound.

The next catalyst needs to come from earnings — and that’s where perception and reality might diverge. There's still a widespread belief that the Mag 7 are fundamentally resilient, high free cash flow generators with strong returns on invested capital. These traits do make them more attractive in a low-growth environment. But we shouldn’t confuse quality business models with true defensiveness.

In reality, many of these companies are still quite cyclical. Meta, for example, is 98% dependent on advertising — which hinges on economic growth. Apple and Tesla are heavily exposed to discretionary spending. Microsoft’s growth is tied to employment trends — fewer new hires mean fewer Office licenses. Even more broadly, communication services and tech sectors have some of the highest shares of imported costs, making them vulnerable to tariffs and supply chain disruptions.

Other risks are lurking too — from mounting regulatory pressures to the possibility that European policymakers could target U.S. tech giants in retaliation against U.S. trade policies.

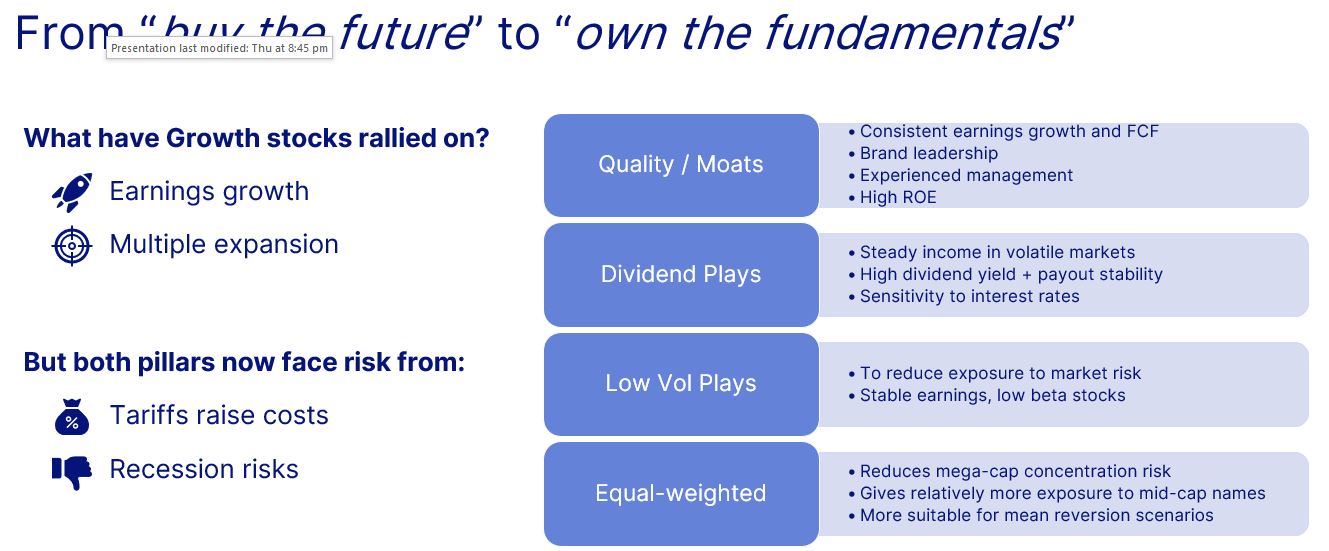

In a world of tariffs, slowing growth, and rising fragmentation, resilience matters more than ever — and not every sector is built for it.

The sectors most vulnerable to a trade war are clear: Consumer Discretionary, Autos, Industrials (even though medium-term reshoring and U.S. reindustrialization can offset), Tech hardware, and Semiconductors. These areas are heavily exposed to global supply chains and cyclical swings.

True resilience means prioritizing companies that can withstand both tariff risks and cyclical slowdowns. Investors should focus on businesses with strong pricing power, domestic and inelastic demand, and solid balance sheets. Supply chains should be less exposed internationally, while demand should be stable regardless of economic conditions.

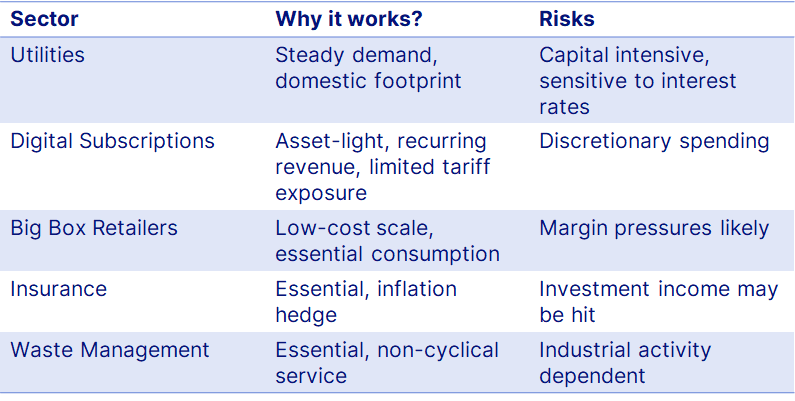

In this environment, quality, stability, and fundamentals should take precedence over chasing flashy trends. Defensive sectors such as Utilities stand out — benefitting from multiple tailwinds: lower energy prices, and rising electricity demand fueled by AI, EVs, and broad electrification. Utilities look interesting not only in the U.S., but also in Europe, where infrastructure buildout is increasingly becoming a strategic priority.

Other sectors to watch for resilience include:

When buying stocks that are down 20–30%, the right way to frame it is from a two-year forward perspective: do you believe you’ll earn healthy returns from here? You might not catch the exact bottom — and you shouldn’t expect a quick V-shaped recovery either. The mindset needed is that things could stay difficult for the next 2–3–6 months, but if you’re investing in a strong business with a proven ability to ride out storms, you’re setting up for longer-term gains.

The U.S. still has no true alternatives when it comes to innovation, balance sheet strength, global reach, and the depth of its financial markets. Investors should use periods of volatility to selectively add high-quality U.S. stocks, especially among the tech giants. Focus less on trying to time the bottom — and more on building long-term exposure to businesses that have consistently delivered through multiple cycles.

As the global cycle fractures and capital rotates, regional diversification becomes critical — and several opportunities stand out. However, there is a key caveat: selectivity is crucial. These are not broad "buy everything" stories. Within each region, investors need to focus carefully on the sectors and themes that are positioned to ride through the next phase of global volatility.

In a fragmented, policy-driven world, thematic investing isn’t just relevant — it’s becoming essential.

Thematic opportunities today cut across sectors, geographies, and even traditional asset classes. Policy-driven megatrends such as AI, robotics, healthcare innovation, supply chain resilience, and the rise of affluent consumers are reshaping the global economy in ways that structural investors cannot afford to ignore.

These themes are not short-term fads. They are backed by long-term capital flows, government support, and shifting global demographics. Whether it's the acceleration of automation, the aging of populations, the rebuilding of critical infrastructure, or the digitization of everyday life, these trends will drive economic value creation over the next decade and beyond.

For investors, thematic exposure offers a way to future-proof portfolios — by positioning around growth vectors that are less dependent on the traditional economic cycle and more aligned with structural shifts. In an environment of higher volatility, slower baseline growth, and geopolitical fragmentation, thematic investing offer targeted, high-conviction opportunities.

The recent simultaneous weakness in U.S. stocks, bonds, and the dollar has rattled investors — and it’s sending a louder message than just economic slowdown fears. Historically, during periods of risk aversion, we would expect equities to sell off, but bonds and the dollar to rally. Instead, we’re now seeing stress across all three — a sign that investors are not just reacting to cyclical risks, but beginning to question the structural foundations of U.S. market leadership.

Initially, the selloff was about fears of a deteriorating real economy. But it has since morphed into something deeper — concerns about fiscal slippage, political pressure on the Fed, and a weakening belief in the U.S. as a rules-based, credible system. When the dollar, long viewed as a haven, weakens alongside stocks and bonds, it reflects a crack in the perception of U.S. assets as universally safe even though markets have stabilized recently.

The bigger issue is no longer just about debt levels — it’s about credibility. U.S. assets have been "safe" because of the belief in a rules-based system, anchored by strong institutions. If that belief cracks, the world will demand a higher premium to hold U.S. debt – and that could fundamentally alter the role of Treasuries and the dollar in global portfolios.

Given the crosscurrents, bond positioning requires selectivity despite risks of an economic slowdown. Short-duration bonds, floating-rate instruments, and inflation-protected securities (TIPS) currently offer the best risk-reward profile. This isn’t the time for broad duration bets or passive exposure. It's about managing interest rate risk carefully and staying flexible in an environment where safe haven status can no longer be taken for granted.

We believe the U.S. dollar still has further to fall. Even after a roughly 5% drop on a trade-weighted basis, the real value of the dollar remains nearly two standard deviations above its long-term average — according to Federal Reserve data. Historically, similar valuation extremes (in the mid-1980s and early 2000s) were followed by broad dollar depreciations of 25–30%.

The catalyst this time isn’t just Fed policy shifts — it’s the broader investment landscape. The U.S. growth advantage relative to the rest of the world is fading. Slower GDP and corporate profit growth, rising political uncertainty, and concerns around Federal Reserve independence make U.S. assets less compelling on a forward-looking basis.

As global investors look to diversify away from U.S. assets, the dollar’s valuation premium is likely to erode. It's not simply about near-term capital flows; the bigger issue is the strategic reallocation of portfolios away from U.S. concentration.

Unless the administration can successfully stabilize labor markets, reinforce Fed credibility, and soften the economic blow from tariffs — a tall order — the dollar’s decline is likely to continue.

Several assets and regions stand to gain. Gold is a clear beneficiary — it acts as a politically neutral, non-yielding asset that historically performs well when the dollar weakens.

Among currencies, we expect European currencies to structurally benefit the most, supported by improving fiscal dynamics and relative undervaluation. Meanwhile, the Swiss farnc and the Japanese yen remain a strong hedge, especially as we start to see harder economic data roll in post-tariffs.

Dollar depreciation should not be mistaken for de-dollarization.

Even with a weaker exchange rate, the dollar’s role as the world’s primary medium of exchange and store of value remains deeply entrenched. Large moves in the dollar have happened before — including multi-decade lows — without meaningfully displacing its dominance in global finance and trade.

Barring an extreme systemic shock, we expect the dollar to retain its leadership position, even if investors continue to diversify at the margins.

The setup for gold remains powerful — and while the short-term outlook may get bumpier, the long-term case remains intact.

Several forces have driven gold’s surge: collapsing real yields, persistent geopolitical risks, and strong central bank buying. Central banks have been accumulating gold for three consecutive years, motivated partly by a desire to hedge against a world where reserve assets can be frozen or weaponized — a reality highlighted by sanctions against Russia. In a fragmented global system, gold’s neutrality and independence from any single country’s creditworthiness have made it a strategic hedge once again.

Beyond central banks, investor demand is rebuilding. ETF and private investment flows are rising, but remain well below 2020-21 levels — suggesting there is still plenty of room for investment demand to catch-up. After being heavily distracted by the equity market boom over the past few years, many investors are now gradually reallocating toward gold, recognizing its value as a hedge against both market volatility and growing geopolitical risks.

That said, while gold has reached our medium-term target of USD 3,500, further upside from here would likely require a renewed worsening of either economic or political conditions. Our long-term view on gold remains positive, but returns may become more event-driven at these higher levels and may need further deterioration of economic or political conditions.

We continue to see five common mistakes:

Volatility is not a reason to abandon a portfolio — it’s a reason to evolve and adapt.

Investors today need a dual focus:

The day-to-day noise can be brutal. But for patient, strategic investors, these are often the foundations for strong future returns.

A resilient portfolio blends flexibility with long-term positioning — designed not just to survive volatility, but to use it as an opportunity.

Here’s a broad framework which blends a strong U.S. core with quality and income, adds global diversification, hedges with real assets, and leans into high-conviction secular themes. And yes — it holds some cash for flexibility when dislocations arise.

Some references are as below:

This framework is intended as a thought starter for building resilient, forward-looking portfolios—not as investment advice.

Outrageous Predictions

Saxo Group

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist