Outrageous Predictions

Révolution Verte en Suisse : un projet de CHF 30 milliards d’ici 2050

Katrin Wagner

Head of Investment Content Switzerland

la Suisse se lance dans une révolution énergétique de CHF 30 milliards d'ici 2050, rivalisant avec l...

Investment and Options Strategist

Résumé: SpaceX options launched on 16 June, and the first thing the market did was buy 65,000 out-of-the-money calls at 200% implied volatility with two days to expiry. That’s not a signal, it's noise. Whether you can tell the difference depends on whether you know what a Day 1 options chain actually looks like. Six professional rules for navigating a brand-new options listing: ...

A new options chain on a stock with no pricing history is structurally different from any established market. Treating it like one is the most common – and most predictable – mistake.

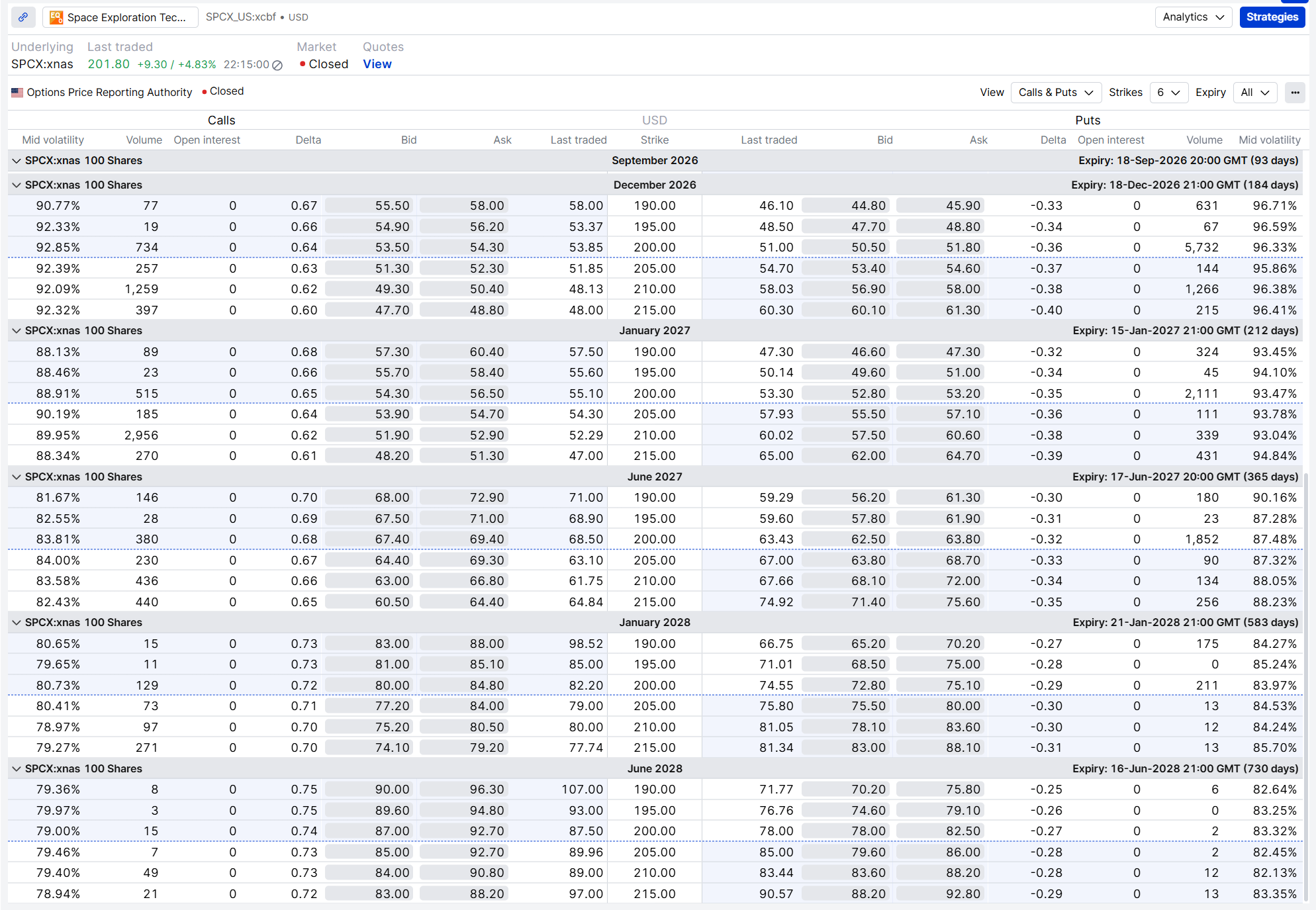

SpaceX priced its IPO at $135 on 12 June 2026. Two trading sessions later, the stock had reached $193 – a gain of 43% against a market capitalisation above $2 trillion. Options began trading on 16 June. By then the stock was near $201.80, still moving. (Source: Saxo platform, SPCX chain data as of 16 June 2026 close.)

What followed is a useful case study for any options trader who encounters a newly listed chain.

Important note: The strategies and examples provided in this article are purely for educational purposes. They are intended to assist in shaping your thought process and should not be replicated or implemented without careful consideration. Every investor or trader must conduct their own due diligence and take into account their unique financial situation, risk tolerance, and investment objectives before making any decisions. Remember, investing in the stock market carries risk, and it’s crucial to make informed decisions.

In a mature options market, implied volatility is anchored by trading history, earnings patterns, sector norms, and accumulated open interest. None of that exists on Day 1. Market makers are pricing from scratch, with only the stock’s own post-IPO moves as a reference point.

For SPCX, the chain opened at approximately 169% implied volatility at the money in the 2-day weekly expiry, declining to 78% at the longest expiry available (∼912 days). A 91 percentage-point spread across the term structure, front to back, with no historical data behind any of it. (Source: Saxo platform, SPCX chain data as of 16 June 2026 close.)

The practical point: do not anchor to Day 1 implied vol as if it reflects a stable, discoverable fair value. It does not. The opening level reflects structural uncertainty, not a calibrated view of the underlying. It will move significantly in the first days as order flow establishes itself. Treating that opening IV as a sustainable baseline rather than a starting point leads to unrealistic expectations.

The widest spreads and the highest implied vol readings occur at or near the open, when market makers are calibrating against the first waves of order flow. By the afternoon session, spreads have typically narrowed. By the second and third sessions, the picture is clearer still.

For anyone who is not specifically trying to capture opening-hour premium, waiting even a few hours tends to produce more efficient entry. Chasing prices in the first 30 to 60 minutes of a newly listed options market rarely results in fills that look reasonable later the same day.

This was visible in the SPCX chain on Day 1: the at-the-money options in the nearest monthly expiry ran 1.5 to 2.5% spread relative to mid later in the session. Two strikes out of the money, spreads widened to 4% or more before the position had done anything. (Source: Saxo platform, SPCX chain data as of 16 June 2026 close.)

Market orders in a thin, newly listed options market can fill at prices that look very different from the quoted mid. Setting a limit price – even if it means the order sits unfilled – is standard practice. Paying the ask in a wide-spread market gives up a significant edge before the position has any chance to work.

A failed fill at mid-price is information. It tells you the real market is not where the screen shows. Use it. Do not respond by improving the price.

In an established options market, large open interest concentrations create gamma exposure that can influence intraday price action. Dealer hedging flows tie themselves to specific strikes. Traders watch the Call Wall and Put Wall. That entire structure takes weeks to develop.

On Day 1 of SPCX options, open interest was zero across the entire chain – every expiry, every strike. Intraday movement in the stock was driven by equity order flow, not options market structure. There was no GEX profile, no meaningful skew to reference, and no gamma exposure to anticipate. Applying options-market-structure analysis to a Day 1 chain produces answers that are not wrong so much as simply not available yet.

The shortest available expiry holds the highest implied volatility, the fastest theta decay, and the most concentrated event risk – and on a hot IPO, the most retail speculation.

On SPCX Day 1, the 2-day weekly (June 18 expiry) was by far the most active in the chain. But the volume was almost entirely OTM calls: the 220-strike traded 64,893 contracts, the 210-strike 63,425, the 250-strike 54,140. These contracts were priced at implied volatilities between 172% and 244% with two days to expiry. The traders buying them needed the stock to move sharply higher, immediately. That is a bet, not a position. (Source: Saxo platform, SPCX chain data as of 16 June 2026 close.)

The June 18 expiry was also the last trading day before Juneteenth (19 June, NYSE closed), further compressing the effective window for those contracts. None of this is obvious from looking at the chain; it requires knowing the context.

As a structural principle, and in our view, starting with a slightly further-dated expiry tends to reduce day-to-day noise while the chain finds a stable pricing regime. The medium-term window is where most systematic traders will eventually find the better risk/reward – but on Day 1 of SPCX, even the 65–93-day expiries (August and September) were largely bypassed by the market, with volume scattered thinly across a handful of strikes.

The chain will develop. Open interest will build. A proper term structure, a skew profile, and a gamma map will emerge over the coming weeks. These are the tools worth waiting for:

Put/call ratio – becomes meaningful once open interest reflects real positioning, not just Day 1 curiosity.

Skew – in the SPCX chain, put IV and call IV were roughly symmetric at the money in the shortest expiry. In the longer-dated expiries, put IV already exceeded call IV by three to five points – the market beginning to price downside protection as the horizon extends. Watching that develop across all expiries as trading matures is more informative than any single-day snapshot.

Structured catalysts – lock-up expiry, first earnings, index inclusion. These are dateable events the inverted term structure is already pricing for. They are where a position can be built with a clear thesis and a known calendar. Those opportunities do not exist yet. They will.

In our view, the consistent professional reflex when a glamour name starts trading options is: wait. Not because there is no opportunity in a new chain, but because patience in the first days has a consistently positive track record against the alternative of chasing the opening move at peak spread and peak implied volatility.

The SPCX chain on Day 1 showed what the alternative looks like: tens of thousands of OTM call contracts at 170 to 244% implied volatility with 48 hours left. Those traders are in a different game. For most systematic options practitioners, the better entry point comes when the market finishes discovering its own price – and the structural tools needed to navigate it are actually in place.

| Related articles/content |

|---|

| What IV crush really means in practice reviewed version | 9 April 2026 Trading earnings with defined | 31 Mar 2026 After the Nasdaq shock three QQQ option strategies for three market views | 9 June 2026 PayPal earnings trading the expected move with options | 4 May 2026 ArcelorMittal earnings what a 10 options move can teach traders | 28 April 2026 ASML earnings is the 8 move already priced in | 10 April 2026 ASML earnings - how to think about the setup before the numbers | 10 April 2026 Options Brief - Mag 7 earnings night Fed holds - 29 April 2026 Options Brief - Mag 7 earnings on deck - 28 April 2026 Options Brief - Oil jolt - US records - 23 April 2026 |

| More from the author |

|---|

Weather risk returns as El Niño threatens crops, grids and mines

Outrageous Predictions

Head of Investment Content Switzerland

Outrageous Predictions

Senior Relationship Manager

Outrageous Predictions

Saxo Group

Outrageous Predictions

Global Head of Macro Strategy

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Chief Investment Strategist

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Global Head of Investment Strategy

Outrageous Predictions

Investor Content Strategist

Outrageous Predictions

Global Head of Macro Strategy