Key points:

- Macro: Bessent highlights that tariff de-escalation lies with China

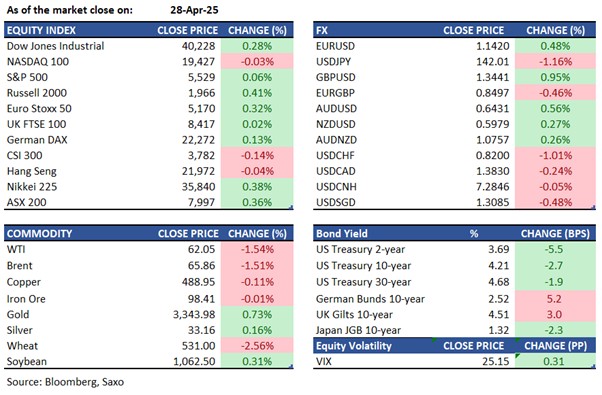

- Equities: S&P 500 rose 0.1%, Hang Seng closed flat in slow trading day

- FX: The pound reached its highest level in three years

- Commodities: WTI fell 1.5% to close near $62, a two-week low

- Fixed income: Treasuries' front end continues to lead gains

------------------------------------------------------------------

Disclaimer: Past performance does not indicate future performance.

Macro:

- US Treasury Secretary Bessent urged China to de-escalate, stating that 145% tariffs are unsustainable and he prefers not to use prepared measures. He noted Chinese exemptions suggest a desire for trade de-escalation and mentioned 15-18 key trade negotiations, including with China, where good proposals have been made, though China's situation is complex, according to CNBC.

- The April Dallas Fed’s business activity index for Texas manufacturing fell 19.5 points to -35.8, it's lowest since May 2020. Production decreased to 5.1, new orders to -20.0, shipments to -5.5, and capacity utilization to -3.8. The company outlook index dropped to -28.3, while uncertainty rose to 47.1.

- In April 2025, the CBI's UK retail sales gauge rose to -8, it's highest in six months, exceeding expectations and improving from -41 in March. However, the May outlook dropped to -33, the lowest in over a year. Despite slower declines, firms are concerned about weak consumer sentiment and global uncertainty. Retailers urge government action to boost confidence, as no sales recovery is expected.

- Mexico's trade surplus rose to $3.44 billion, surpassing expectations. Exports increased by 9.6% to $55.5 billion, driven by accelerated shipments ahead of US tariffs. Non-oil exports grew 9.7%, with notable rises in mining products (+34.1%), manufactured goods (+10%), and machinery (+50.2%). Car exports were up 6.2%, with US sales increasing 6.5% and other markets 4.0%.

Equities:

- Market is closed in Japan

- US - US stocks ended mixed on Monday as Wall Street anticipated a busy week of major earnings and crucial economic data. The S&P 500 rose 0.1%, and the Dow Jones gained 0.3%, both marking a fifth straight day of gains, while the Nasdaq 100 fell 0.1% despite a late rebound in Big Tech. Investors focused on upcoming earnings from Amazon, Apple, Meta Platforms, and Microsoft, and watched for effects of President Trump's tariffs on corporate outlooks. Although earnings largely exceeded expectations, tariff uncertainty led many companies to lower second-quarter guidance. Treasury Secretary Scott Bessent emphasised that reducing trade tensions was "up to China," while noting progress on other trade issues.

- EU - European stocks advanced on Monday, with the Stoxx 50 up 0.2% and the Stoxx 600 rising 0.5%, as all sectors saw gains. Automotive and banking stocks led with 0.7% increases. Investors are anticipating key earnings from Porsche, Schneider Electric, and Deutsche Boerse amid easing trade tensions. In corporate news, Italy’s Mediobanca (+0.8%) launched a €6.3 billion bid for Banca Generali (+7.5%) to enhance its wealth management operations. Additionally, Airbus (+1.8%) completed a deal to acquire key assets from Spirit AeroSystems, bolstering its European aircraft production capabilities. In Germany, healthcare and materials firm Merck announced an agreement to purchase U.S. biotech company SpringWorks Therapeutics, with an equity value of $3.9 billion, to enhance its cancer drug portfolio.

- HK - The Hang Seng closed flat at around 21,981 on Monday, as traders absorbed the press briefing in China after Friday's Politburo meeting. Officials pledged support for exporters and workers impacted by U.S. tariffs and prepared contingency measures for China's broader economy. Early losses in the session were offset by gains in financials and tech, balancing declines in property and consumer sectors, as Beijing held off on new stimulus, preferring to act as the situation unfolds. Meanwhile, U.S. futures dipped slightly after Treasury Secretary Bessent did not endorse President Trump's claim of active tariff talks with China. Beijing granted exclusions on some U.S. imports previously subject to 125% tariffs. Akeso Inc. (-11.8%) and BYD Electronic (-8.6%) declined, while Pop Mart Intl. (+12.1%), China State Construction (+6.0%), and SITC Intl. (+4.0%) gained.

Earnings this week:

Tuesday: Coca-Cola, Starbucks, Booking, Royal Caribbean, Norwegian Cruise, Spotify, Visa, UPS, Mondelez

Wednesday: Microsoft, Meta, Robinhood, Qualcomm, eBay

Thursday: Apple, Amazon, Block, CVS, Mastercard, Hershey

Friday: Exxon, Chevron

FX:

- The dollar weakened after a poor manufacturing report raised US growth concerns. The pound hit a three-year high, while the yen and Swiss franc rose over 1%. The Bloomberg Dollar Spot Index fell 0.4%.

- USDJPY dropped 1.1%, USDCHF fell 1%, and EURUSD rose 0.5% with the ECB considering lower borrowing costs. JPMorgan raised its euro forecast.

- GBPUSD rose nearly 1% to its strongest since February 2022.

- USDCAD fell 0.3%. Trump repeated comments about Canada becoming the 51st US state as Canadians voted.

- AUDUSD held most of Monday's gains amid dollar weakness, following the US Treasury Secretary's call for China to de-escalate the trade war.

- Economic data: US goods trade, job openings & Conference Board consumer confidence, Eurozone consumer confidence

Commodities:

- Oil steadied after a drop, with US economic strain from the trade war and Iran talks. WTI was near $62, and Brent crude below $66. US manufacturing weakened, showing tariff impacts, with more economic data coming soon.

- Copper remains stable with a three-week gain, driven by rising demand in China. China's metals markets show strong copper drawdowns and low zinc and aluminium stockpiles. Officials aim to boost economic support, while the US calls for tariff easing by Beijing.

- Gold rose as the dollar and bond yields fell, with traders anticipating key economic data on jobs, inflation, and growth from Wednesday to Friday. Gold is up over 25% this year due to Trump's trade policy and global economic fears boosting demand for safe assets.

Fixed income:

- Treasuries climbed, with yields down up to 7 basis points, steepening the curve. Early stock weakness and falling oil prices contributed, with the next auction on 5 May. Yields fell 1 to 7 basis points; the US 10-year yield dropped about 3 basis points, outperforming European bonds.

For a global look at markets – go to Inspiration.